When people hear the word bankruptcy, they often think of failure. In reality, bankruptcy is a federal legal system designed to balance two fundamental goals:

- Provide honest debtors with a fresh start

- Ensure fair and orderly treatment of creditors

Whether you’re an entrepreneur, investor, or individual facing financial distress, understanding bankruptcy law transforms fear into strategy.

What Is Bankruptcy?

Bankruptcy is a legal proceeding involving a person or business that cannot repay outstanding debts. Most cases begin with a voluntary petition filed by the debtor. In limited circumstances, creditors may file an involuntary petition (typically under Chapter 7 or Chapter 11) against an eligible debtor.

In the United States, bankruptcy cases are handled in federal courts under the U.S. Bankruptcy Code.

Bankruptcy is not punishment. It is a structured legal process that:

- Provides relief from collection pressure

- Protects certain assets

- Establishes a fair system for distributing remaining assets

1. Who Can File Bankruptcy?

Bankruptcy relief is available to:

- Individuals

- Married couples (joint filing permitted)

- Sole proprietors

- Partnerships

- Corporations

- Limited liability companies (LLCs)

Basic Requirements

To file bankruptcy, you must:

- Reside, have a domicile, or conduct business in the United States

- Complete required credit counseling (generally within 180 days before filing)

- Meet eligibility requirements for the specific chapter

Repeat filings are possible but may limit the automatic stay or discharge depending on timing.

2. Common Causes of Bankruptcy

Financial distress often results from multiple factors:

- Medical expenses (frequently cited as a major contributor)

- Job loss or reduced income

- Business failure

- Divorce or family disruption

- Excessive leverage

- Unexpected emergencies

Bankruptcy is usually about cash-flow breakdown, not irresponsibility.

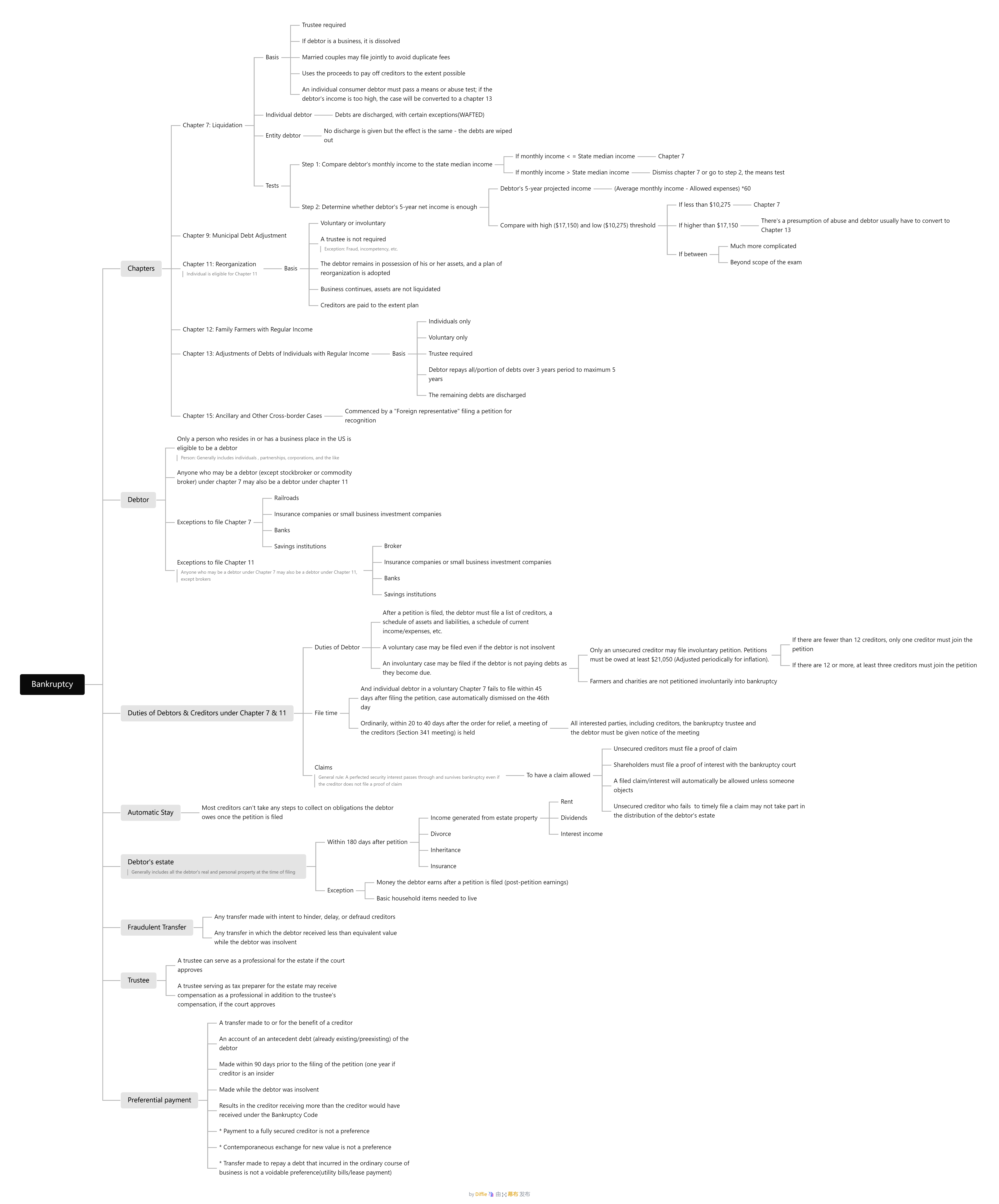

3. The Most Common Bankruptcy Chapters

Chapter 7 – Liquidation (“Fresh Start”)

Chapter 7 eliminates many debts through liquidation of non-exempt assets.

Characteristics

- Voluntary or involuntary

- Trustee required

- If debtor is a business, it is dissolved

- Married couples may file jointly to avoid duplicate fees

- Uses the proceeds to pay off creditors to the extent possible

- An individual consumer debtor must pass a means or abuse test; if the debtor’s income is too high, the case will be converted to a chapter 13

Who is not eligible:

- Railroads

- Insurance companies or small business investment companies

- Banks

- Savings institutions

The Chapter 7 Means Test — Detailed Breakdown

To prevent abuse, consumer debtors must pass a statutory means test.

Step 1: State Median Income Comparison

The debtor’s current monthly income is compared to the state median income for a household of the same size.

- If income is less than or equal to the state median → Generally eligible for Chapter 7.

- If income is greater than the state median → Proceed to Step 2.

Step 2: 5-Year Disposable Income Calculation

If income exceeds the median, projected disposable income over five years must be calculated:

(Average Monthly Income – Allowed Expenses) × 60

Outcomes:

- Below lower threshold ($10,275) → Eligible for Chapter 7

- Above upper threshold ($17,150) → Presumption of abuse; case typically converted to Chapter 13 or dismissed

- Between thresholds → More detailed statutory analysis required, not in CPA exam scope

Passing the means test does not guarantee discharge, and failing it does not eliminate relief. It often shifts the case to Chapter 13.

Debts Generally Not Discharged in Chapter 7

- W – Willful and malicious injury: Debts arising from intentional harm caused to another person or their property.

- A – Alimony: Spousal support and child support obligations.

- F – Fraud: Debts incurred through fraud, embezzlement, or larceny, as well as certain fines and penalties owed to government agencies.

- T – Taxes: Certain types of unpaid taxes, particularly those due within three years of the bankruptcy filing.

- E – Educational loans: Student loans, which are generally not discharged unless the debtor can prove “undue hardship.”

- D – Debts undisclosed: Any debts that the debtor failed to list or “schedule” in their bankruptcy petition, preventing the creditor from participating in the case.

Chapter 9 – Municipal Debt Adjustment

Only a municipality may file.

Under the Code, a municipality includes:

- Cities

- Counties

- Towns

- Villages

- Public school districts

- Public utility districts

- Other political subdivisions or public agencies

Chapter 11 – Reorganization

Primarily used by businesses. Individuals are eligible too.

Characteristics

- Voluntary or involuntary

- Trustee is not required except fraud, incompetency etc.

- Debtor remains in control (“debtor in possession”)

- Reorganization plan proposed

- Creditors vote

- Business continues operating

Allows restructuring, contract rejection, and preservation of enterprise value.

Who is not eligible:

- Broker

- Insurance companies or small business investment companies

- Banks

- Savings institutions

Chapter 12 – Farmers & Fishermen

Only family farmers or family fishermen who meet statutory requirements may file. Both individuals and family-owned corporations or partnerships may qualify.

A debtor must:

- Be engaged in a farming operation

- Have regular annual income

- Have total debts below a statutory cap (adjusted periodically)

- Have a specified percentage of debts arising from farming operations

- If an individual, receive a majority of gross income from farming

Chapter 13 – Adjustments of Debts of Individuals with Regular Income

Designed for individuals with regular income.

Characteristics

- Individuals only

- Voluntary only

- Trustee required

- Debtor keeps property

- 3–5 year repayment plan

- Remaining eligible debt discharged after completion

Often used to stop foreclosure or protect non-exempt assets.

Chapter 15 – Ancillary and Other Cross-border Cases

Commenced by a “Foreign representative” filing a petition for recognition.

- A foreign company has filed insolvency proceedings in another country

- The debtor has assets, creditors, or litigation in the United States

- A foreign representative seeks U.S. court assistance

It is common in multinational corporate restructurings.

4. Automatic Stay — Immediate Protection

Upon filing, an automatic stay takes effect immediately.

It:

- Stops lawsuits

- Halts collections

- Prevents foreclosure

- Stops wage garnishment

- Pauses repossession

- May temporarily halt eviction (subject to exceptions)

It prevents a race to collect and gives breathing room.

5. Bankruptcy Estate

Generally including all the debtor’s real and personal property at the time of filing:

- Real estate

- Personal property

- Bank accounts

- Investments

- Certain income gained within 180 days

- Income generated from estate property

- Rent

- Dividends

- Interest income

- Divorce

- Inheritance

- Insurance

- Income generated from estate property

Exemptions:

- Money the debtor earns after a petition is filed (post-petition earnings)

- Basic household items needed to live

6. The Trustee’s Role

Trustees:

- Liquidate non-exempt assets

- Review disclosures

- Conduct the 341 meeting

- Pursue avoidance actions

- Distribute funds by priority

- Object to improper discharges

They act for creditors, not the debtor.

- A trustee can serve as a professional for the estate if the court approves

- A trustee serving as tax preparer for the estate may receive compensation as a professional in addition to the trustee’s compensation, if the court approves

7. Avoidance Powers

Preferential Transfers

Trustee may recover transfers:

- To a creditor

- For a pre-existing debt

- Made while insolvent

- Within 90 days (1 year for insiders)

- That allowed greater recovery than Chapter 7 distribution

Purpose: prevent favoritism.

Exceptions:

- Payment to a fully secured creditor is not a preference

- Contemporaneous exchange for new value is not a preference

- Transfer made to repay a debt that incurred in the ordinary course of business is not a voidable preference (utility bills/lease payment)

Fraudulent Transfers

Transfers made:

- With intent to hinder or defraud creditors

- For less than reasonably equivalent value while insolvent

May be reversed.

8. Claims & Priority

Not all creditors are treated equally.

Order of Payment:

- Secured creditors (to extent of collateral)

- Administrative expenses (trustee, attorneys)

- Priority unsecured claims (taxes, child support)

- General unsecured creditors

- Equity holders (rarely receive anything)

This hierarchy explains why equity is typically wiped out in insolvency.

9. Duties of the Debtor

Debtors must:

- File complete financial disclosures

- List all assets and liabilities

- Attend 341 meeting of creditors

- Complete financial education course

- Cooperate with trustee

Failure may result in dismissal or denial of discharge.

10. After Bankruptcy

Credit Reporting

- Chapter 7: up to 10 years

- Chapter 13: up to 7 years

Rebuilding

Many rebuild credit within several years through responsible borrowing and stable income.

11. Bankruptcy Myths

Myth: You lose everything.

Fact: Exemptions protect essentials.

Myth: All debts disappear.

Fact: Some survive discharge.

Myth: You’ll never get credit again.

Fact: Many rebuild within years.

Final Takeaway

Bankruptcy is:

| Tool | Function |

|---|---|

| Automatic Stay | Immediate protection |

| Estate Creation | Centralized asset management |

| Means Test | Chapter filter |

| Priority Rules | Fair distribution |

| Discharge | Fresh start |

| Reorganization | Business restructuring |

Bankruptcy is not the end. It is a structured reset mechanism within a credit-based economy.

Mindmap made by Diffie:

Disclaimer: This article provides general information about bankruptcy law and does not constitute legal advice. Bankruptcy laws vary by jurisdiction and are subject to change. Consult with a qualified bankruptcy attorney regarding your specific situation.

Leave a comment